← Back to catalog

Pack · 3 sessions

ORB System

All three ORB strategies running together as one system: Asian (gold), European and US sessions. Cross-session diversification for a portfolio more robust than any single strategy.

⏳ In validation — available soon

The pack opens once the three strategies build ~2 months of combined live track record (expected end of August 2026). The combined live record starts on 06/24/2026.

Join the waitlistHow it works

ORB System is not a new strategy: it is the three ORB strategies you already know —Asia (gold), Europe and the US— running together as a single portfolio. Each trades its own session, in its own time window and, for gold, on a different instrument.

Why they work better together than apart. The three sessions barely overlap in time and behave independently: in the backtest, the correlation between them is practically zero. So when one goes through a flat patch, the others don't have to follow. As a result, the drawdown of the combined portfolio is lower than that of any of the three on its own: the dips of one are offset by the others, and the combined curve is smoother and more stable.

Real diversification, not stacked risk. Adding strategies only reduces risk when they are genuinely independent. Here they are: different time window, different session and, for gold, a different market. That is why the full system aims for a more robust profile than trading a single one.

🟢 Live account · in progress

Live Account Results (Live Trading)

Real trades with real money (account 1075993). Still a small sample — these figures build up gradually and the history grows every week. The full trade-by-trade record is on the results page.

83.33%

Winning trades (small sample)

22.10

Profit factor (small sample)

📊 Backtest Results (Historical Simulation)

⚠️ Hypothetical simulated results. These are not real results. The backtest runs the strategy over historical price data. See the hypothetical results disclosure in the footer.

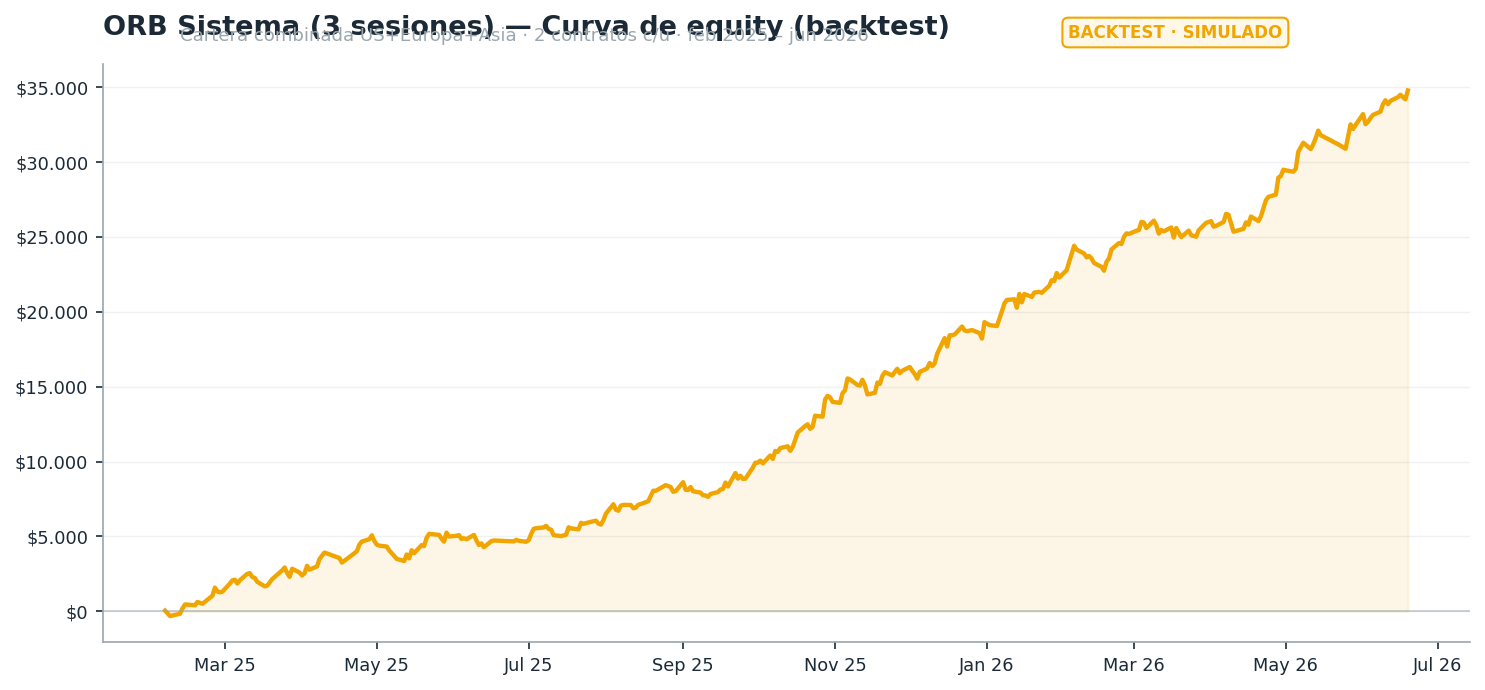

Period: Feb 2025 — Jun 2026 • Instrument: MNQ + MGC • Timeframe: 5 min • 2 contracts per strategy

Total net profit:$34,781.50

Profit factor:1.74

Max drawdown:$-1,715.00

Combined operations: 620 • Win rate:60.5%

⚠️ Cumulative profit curve — SIMULATED BACKTEST

Why the full system is more robust

Three independent sessions (Asia, Europe, US) in one portfolio

Practically zero correlation between strategies → real diversification

Combined drawdown lower than any of the three alone

Smoother, more stable combined curve

No overnight exposure in any session

Get it

⏳ Waitlist

Lifetime access (all 3)

2,997€ + VAT

(~$3.518 USD)

One-time payment — includes all three

Join the waitlist— or —

Monthly subscription (all 3)

247€/mo + VAT

(~$290 USD/mo)

Manual renewal — cancel anytime

Waitlist (monthly)⚠️ The pack is not on sale yet: in validation. Only a NinjaTrader 8 software license is sold. We are not financial advisors. Past results do not guarantee future results.

Risk Disclosure: Futures and forex trading involves substantial risk and is not appropriate for all investors. An investor could potentially lose all or more than the initial investment. Risk capital is money that can be lost without jeopardizing one's financial security or lifestyle. Only risk capital should be used for trading and only those with sufficient risk capital should consider trading. Past results are not necessarily indicative of future results.

Hypothetical Performance Disclosure: Hypothetical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect actual trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all of which can adversely affect actual trading results.

NinjaTrader® NinjaTrader® is a registered trademark of NinjaTrader Group, LLC. No NinjaTrader company has any affiliation with the owner, developer, or provider of the products described here, nor has any interest in, or provides any recommendation for the products or services described.