ORB — Opening Range Breakout

Operates at the New York market open. Detects trend direction, momentum and breakout of the day's high/low range. 59% win rate in backtest.

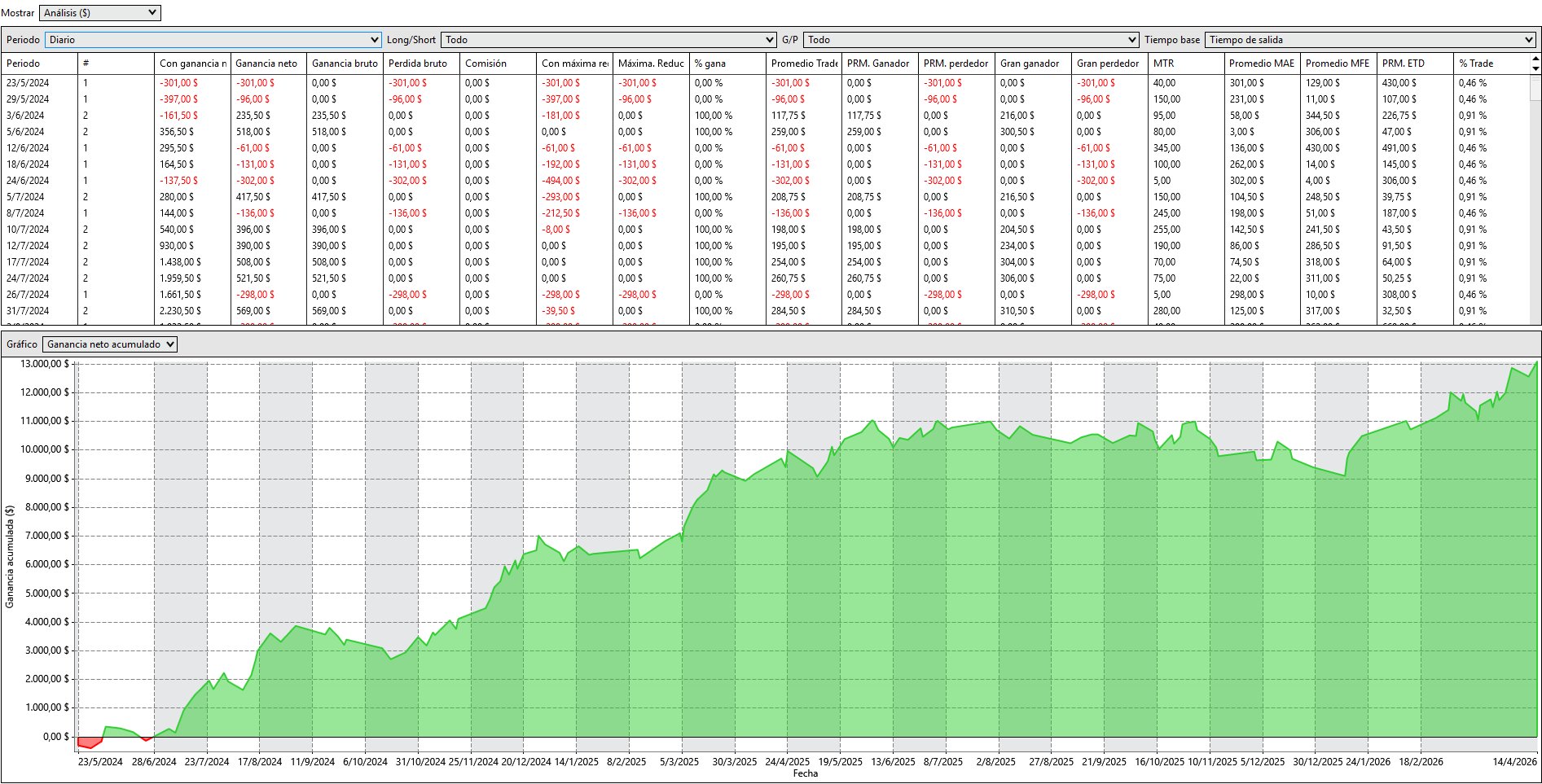

📊 See real results on a live account with real money ↓

The strategy identifies the price range during the first minutes after the New York open. When price breaks that range with sufficient momentum and in the direction of the day's trend, it automatically enters the trade. The exit is managed through predefined targets and dynamic stops.

Live Account Results

These are not simulations. They are trades executed automatically by the ORB strategy on a live account with real money (account 1075993). Every trade is logged with its exact timestamp and price.

Period: 01/01/2026 — 13/06/2026 · Instrument: MNQ/NQ · Timeframe: 5 min · 2 contracts

Indicative capital based on MNQ backtest history. Always trade within your own risk management.

Important: past backtest results do not guarantee future results. The ORB is a strategy with solid logic and reasonable backtest results, but like any trading strategy it can have drawdown periods and may perform differently in changing market conditions. Risk management and position sizing are as important as the strategy itself.

How ORB automation works in NinjaTrader 8

ORB (Opening Range Breakout) starts from a simple idea: in the first minutes after the New York open the bulk of the day's volume and volatility concentrates, and the range that forms in that window tends to mark the levels price respects or breaks during the session. The strategy defines that opening range automatically and watches for a breakout with momentum in the direction of the day's trend. All the logic runs on its own inside NinjaTrader 8.

Why a regime filter (EMA, ADX, ATR). Not every day is tradeable. A breakout in a sideways, directionless or low-volatility session is almost always a trap. Before trading, the strategy reads the context: trend with an exponential moving average (EMA), move strength with ADX and available volatility with ATR. If the context doesn't line up, it doesn't trade. This has an honest cost: there are whole sessions with no trade at all —including some that would have worked— and that is on purpose. We would rather miss a few good ones than take the many bad ones.

Why breakout confirmation, not the first touch. The edge of the range is exactly where stops pile up and where price fakes moves to hunt them. So the entry requires the breakout to confirm before firing, rather than entering on the first tick that touches the level. You give up a little entry price in exchange for filtering out most false starts.

Why managed orders and not «on bar close». The stop, targets and breakeven are placed and managed in real time, reacting to price movement, not only when a candle closes. The reason is practical: a target or stop can be hit mid-candle; if the logic is only evaluated at the close, the real result drifts from what the strategy intended. Managing on price makes live execution match the actual rules.

How the backtest relates to live execution. The backtest’s entry mechanics are built conservatively: the signal is recorded on confirmation, somewhat later than it may fire live. That specific bias works in your favor. But other factors work against you, and no backtest fully captures them: stop slippage on fast moves, each broker’s commissions, or gaps. Live results can land above or below the simulation, and the real drawdown can be larger than the backtested one. That is why we publish both —backtest and real trades, each clearly labeled— so you can make the comparison yourself.

Management: stop, two partial targets and breakeven. The position is managed in parts: it banks profit at a first target and moves the stop to breakeven, so a trade that has already gone in your favor cannot turn into a loss; the rest is left to run toward a second target to capture the larger moves. It is a balance between locking in and letting winners breathe.

No window dressing. ORB is selective, intraday and with no overnight exposure. It does not trade every day, it has losing streaks like any system, and it can underperform if the kind of market it is built for disappears for a while. It is not magic or universal: it is a tool for a specific context. Past results do not guarantee future results.

Real trades

ORB is traded live, with real money, on a verified NinjaTrader account (account 1075993). These are not simulations or screenshots: every trade is recorded by the platform itself with its date, time, entry and exit price and result.

The character of the track record is what you would expect from the above: many days with no trade (the filter keeps the strategy out of bad sessions), days with one or two clean trades when there is trend and momentum, and —yes— losing trades that hit their stop without drama. There are flat stretches and there are drawdowns; they are part of any real system and we do not hide them.

We will not give you a figure here that is out of date tomorrow, or a dressed-up curve. What we do is publish the full log, trade by trade, and update it weekly so you can audit it yourself: See the full trade log →

Past results are not indicative of future results. See the full risk disclosures at invermindslu.com/en/risks.

Parameters and configuration

ORB ships deliberately with very few visible settings. Most internal values —the opening-range window, the regime-filter thresholds, the stop and target logic— are fixed inside the strategy. It is not secrecy: those values are part of what has been tested, and leaving them open would just invite over-tuning until results get worse, one of the most common mistakes in automated trading.

What you do control: the number of contracts (your position size, set to your capital and risk management) and a filter-strictness setting —how many context conditions must line up before it trades. More strictness means fewer but higher-quality signals; less strictness, more signals and more noise. It is a selectivity dial, not a magic profit button.

Compatibility: it is built and tested for MNQ/NQ (Nasdaq futures) and works on a fixed timeframe the strategy itself enforces. We do not claim it works on other markets: what is tested is what is tested.

How do I know the results are real and not made up?

The live track record is still short. Why should I trust it?

It has a high win rate, but aren't the average losses bigger than the average wins?

Do you provide the source code?

Is the license tied to one account or machine?

Does it work on funded accounts (Apex, Topstep…)?

Is there a refund if I'm not convinced?

Is ORB an indicator or a complete strategy?

A complete, automated strategy. An indicator draws levels and you decide; ORB reads the context, enters, manages and exits on its own inside NinjaTrader 8. You do not interpret anything or pull the trigger.

Do I need to know how to code?

No. It installs like any NinjaTrader Ecosystem strategy and activates with your license. If you get stuck on installation, we help.

Do I have to sit in front of the screen?

Not to trade —the strategy acts on its own— but NinjaTrader has to be open and connected during the session. Many people use a VPS so they do not depend on their PC, though it is not required.

Does it work on markets other than MNQ?

It is built and tested for MNQ/NQ (Nasdaq futures). We will not tell you it works for everything: what we have not tested, we do not claim. If you want to use it on another instrument, test it in simulation first.

Why doesn't it trade some days?

By design. The regime filter keeps the strategy out of sideways or low-volatility sessions where breakouts tend to fail. A day with no trades is not a failure: often it is the best decision.

What happens in a losing streak?

It comes, like in any system. ORB does not promise to always win; it has drawdowns and flat stretches, and we acknowledge them openly. You can see them with your own eyes in the live log and during the free trial before risking anything.

- Automated vs. manual trading: which fits you? →

- Is automated trading profitable? →

- What is the Opening Range Breakout (ORB)? →

- Bots on funded accounts: what Apex, Topstep and others allow →

- Can a robot pass a NinjaTrader funded challenge? →

- Automated trading on NinjaTrader 8: a practical guide →

- Best automated strategies for MNQ →

- Trading robots and scams: how to tell what's real →